Accounting is a subject that many people are curious about. There are many aspects of accounting. Here, we'll take a look at the basics: accounts, the balance sheet, and double-entry accounting. Then we'll explain why each one is important. What's in an income statement? How do costs get calculated? What is a profit margin? These questions can be answered with a basic understanding of accounting.

Accounts

Accounting involves the recording and analysis of financial transactions as well as summarizing that information. The basic types of accounts are assets and liabilities, which are accounted for by the income statement and balance sheet. Accounts Receivable and Accounts Payable are the company's liabilities. Generally, accrual accounting records financial transactions as they occur. For example, cash change hands at the time accounts payable is the assets of a company. As such revenue is recognized when it has been earned while expenses are recorded when they are incurred. Amortization can be described as a process where debt is reduced by equal payments.

Balance sheet

The Balance Sheet shows assets, liabilities, equity, and shareholder's equity. Assets refer to the assets of the company that are available for sale, lease, or use in providing services. It also includes intangible assets like patents and trademarks. Liabilities refer to the obligations of the company. Equity refers to the original capital investment by the company and any profit made during the year.

Cost accounting

What is cost accounting? This accounting is used to help businesses identify and reduce their costs. Managers can allocate costs by product line, unit of production, or even per hour of labor. This information allows business owners and managers to assess their profit margins against their competition. It is useful to senior management for planning future spending and forecasting finances. Additionally, it aids companies in finding new efficiencies to improve productivity.

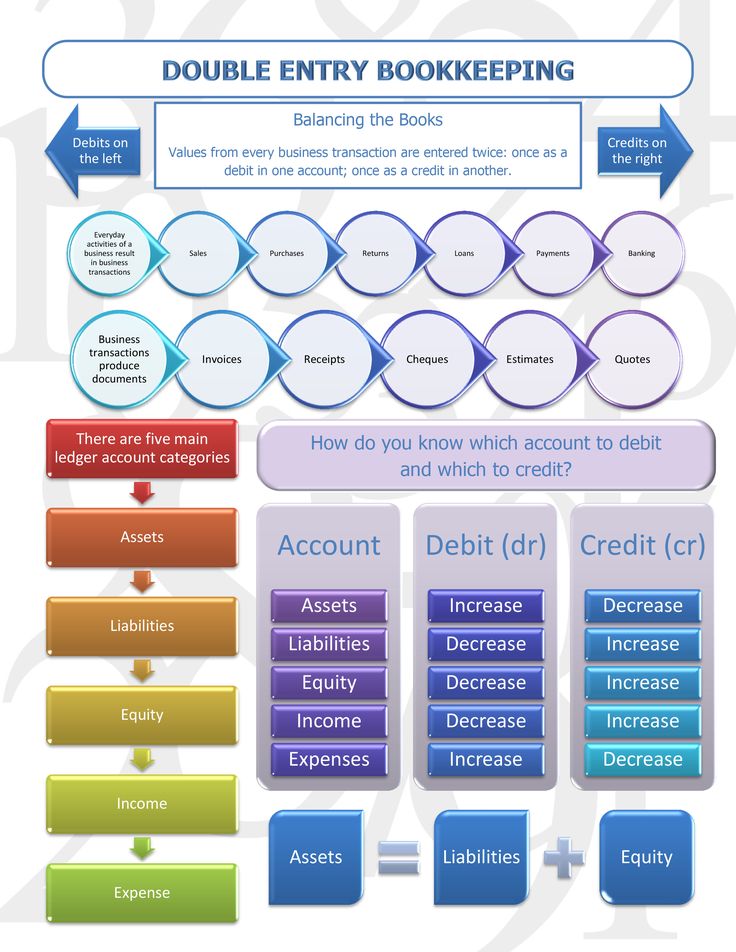

Accounting for double entries

In double-entry accounting, a single transaction triggers a record in both accounts: the general ledger and the balance sheet. The difference is equity. This is the difference between assets and liabilities. Below are examples for double-entry bookskeeping. These examples do not represent the entire process of double-entry accounting. Double-entry accounting requires that you fully understand the rules of double-entry and then apply them accordingly.

Auditing

In the field of accounting, auditing is the process of checking the accuracy of financial statements. A qualified auditor will perform this task. They should have a solid understanding of accounting standards and conventions as well as tax laws. An auditor must be able to detect and assess any fraud or unethical practices within an organization. If a company is involved in a criminal act, the auditor must report this to the relevant authorities.

Taxes

One common misconception about accounting is that it only portrays real-world events. Accounting is a key component of most real-world decisions. Accounting figures allow outsiders to see the economic context of a business transaction. One example is that a company's Balance Sheet may show different effects from different M&A transactions due to different transaction structure. Accounting information is, however the basis for making decisions in many other aspects.

Bookkeeping

What is bookkeeping, exactly? Bookkeeping simply means a system to record, store and report financial information. It's the process of preparing financial reports for your company, such as your income statement and balance sheet. These reports give you a valuable insight into your business' capital and can help you set realistic business goals. You must be familiar with the four types of financial statements that bookkeeping requires: balance sheet, income statement, cashflow statement, cashflow statement and balance sheet.

FAQ

What happens if my bank statement isn't reconciled?

You may not realize you made a mistake until the end of the month if you don't reconcile your bank statements.

At this point, you will need repeat the entire process.

What is bookkeeping and how do you define it?

Bookkeeping can be described as the keeping of records about financial transactions for individuals, businesses and organizations. It includes recording all business-related expenses and income.

Bookkeepers track all financial information such as receipts, invoices, bills, payments, deposits, interest earned on investments, etc. They also prepare tax reports and other reports.

Why is reconciliation important

It's vital as mistakes may happen, and you don't know what to do. Mistakes include incorrect entries, missing entries, duplicate entries, etc.

These problems can have grave consequences, including incorrect financial statements or missed deadlines, overspending and bankruptcy.

What does an auditor do?

Auditors look for inconsistencies between financial statements and actual events.

He checks the accuracy of the figures provided by the company.

He also verifies the validity of the company's financial statements.

How does an accountant do their job?

Accountants work closely with their clients to make sure they get the most from their money.

They work closely alongside professionals like bankers, attorneys, auditors and appraisers.

They also assist internal departments such as human resources, marketing, sales, and customer service.

Accountants are responsible in ensuring that books are balanced.

They determine the tax due and collect it.

They also prepare financial statements, which reflect the company's financial performance.

What kind of training does it take to be a bookkeeper

Basic math skills are required for bookkeepers. These include addition, subtraction and multiplication, divisions, fractions, percentages and simple algebra.

They need to also be able and confident in using a computer.

A majority of bookkeepers hold a high school diploma. Some even have college degrees.

How long does an accountant take?

Passing the CPA test is essential in order to become an accounting professional. Most people who want to become accountants study for about 4 years before they sit for the exam.

After passing the exam, you must work at least three years as an associate to become a certified public accountant (CPA).

Statistics

- a little over 40% of accountants have earned a bachelor's degree. (yourfreecareertest.com)

- BooksTime makes sure your numbers are 100% accurate (bookstime.com)

- Given that over 40% of people in this career field have earned a bachelor's degree, we're listing a bachelor's degree in accounting as step one so you can be competitive in the job market. (yourfreecareertest.com)

- In fact, a TD Bank survey polled over 500 U.S. small business owners discovered that bookkeeping is their most hated, with the next most hated task falling a whopping 24% behind. (kpmgspark.com)

- "Durham Technical Community College reported that the most difficult part of their job was not maintaining financial records, which accounted for 50 percent of their time. (kpmgspark.com)

External Links

How To

How to do Bookkeeping

There are many types of accounting software available today. While some are free and others cost money, most accounting software offers basic features like invoicing, billing inventory management, payroll processing and point-of-sale. The following is a brief overview of the most widely used types of accounting software.

Free Accounting Software - This free software is often offered to personal use. Although it may not have all the functionality you need (e.g., you can't create your own reports), it is easy to use. If you are interested in analyzing your business' numbers, many programs allow you to directly download data to spreadsheets.

Paid Accounting Software is for businesses with multiple employees. They typically include powerful tools for managing employee records, tracking sales and expenses, generating reports, and automating processes. Many companies offer subscriptions with a shorter duration than six months, but most paid programs require a minimum subscription of at least one year.

Cloud Accounting Software - Cloud accounting software lets you access your files via the internet from any device, including smartphones and tablets. This program has been growing in popularity because it reduces clutter and saves space on your computer's hard drive. You don't even have to install any extra software. All that is required to access cloud storage services is an Internet connection.

Desktop Accounting Software: Desktop accounting software is similar to cloud accounting software, except that it runs locally on your computer. Desktop software works in the same way as cloud software. It allows you to access files from any location, including via mobile devices. However, unlike cloud-based software, desktop software must be installed on your computer before it can be used.

Mobile Accounting Software: This mobile accounting software was specifically developed to work on tablets and smartphones. These programs make it easy to manage your finances wherever you are. These programs are typically less functional than full-fledged desktop software, but they can still be useful for people who travel frequently or need to run errands.

Online Accounting Software is specifically designed for small businesses. It has all the features of a traditional desktop software package, but with a few additional bells and whistles. Online software does not need to be installed. Just log in and you can start using it. You can also save money and avoid the overheads of a local office.