New York City's average accountant income is $65,615 USD a year. This is the highest salary in the United States. Women earn an average income of $42,011 and men $62,516 respectively. Eighteen salary surveys revealed that the highest-paid Accountant was paid with a Masters' Degree while the lowest earner earned a Bachelor’s degree.

Average salary

New York City's average salary for an accountant is $89210 per one year. But there are variations. Numerous New York City-based firms employ large numbers of accountants. An entry-level staff accountant can earn around $36,000 per year while more experienced cost accountants can make about $47,000 per year. Senior-level accountants can make as much as $71,340 a year.

Salary Survey's website provides an overview of the average annual salary for Senior Accountants in New York City in 35 languages. A New Yorker with a Master's Degree in Accounting can expect to make $90,000.

Outlook for the Job

You can start networking and building your network today if you are looking for an accounting job in New York City. There are many job opportunities for accountants. The market is highly competitive and you need to stand out to be hired.

More companies will need accountants to manage their financial accounts as the world economy becomes more interconnected. Accounting professionals who are skilled in international trade, mergers and acquisitions will be more needed due to globalization. Complex tax laws will drive further demand for accountants. The demand for accountants could be particularly strong in the technology and international trade industries.

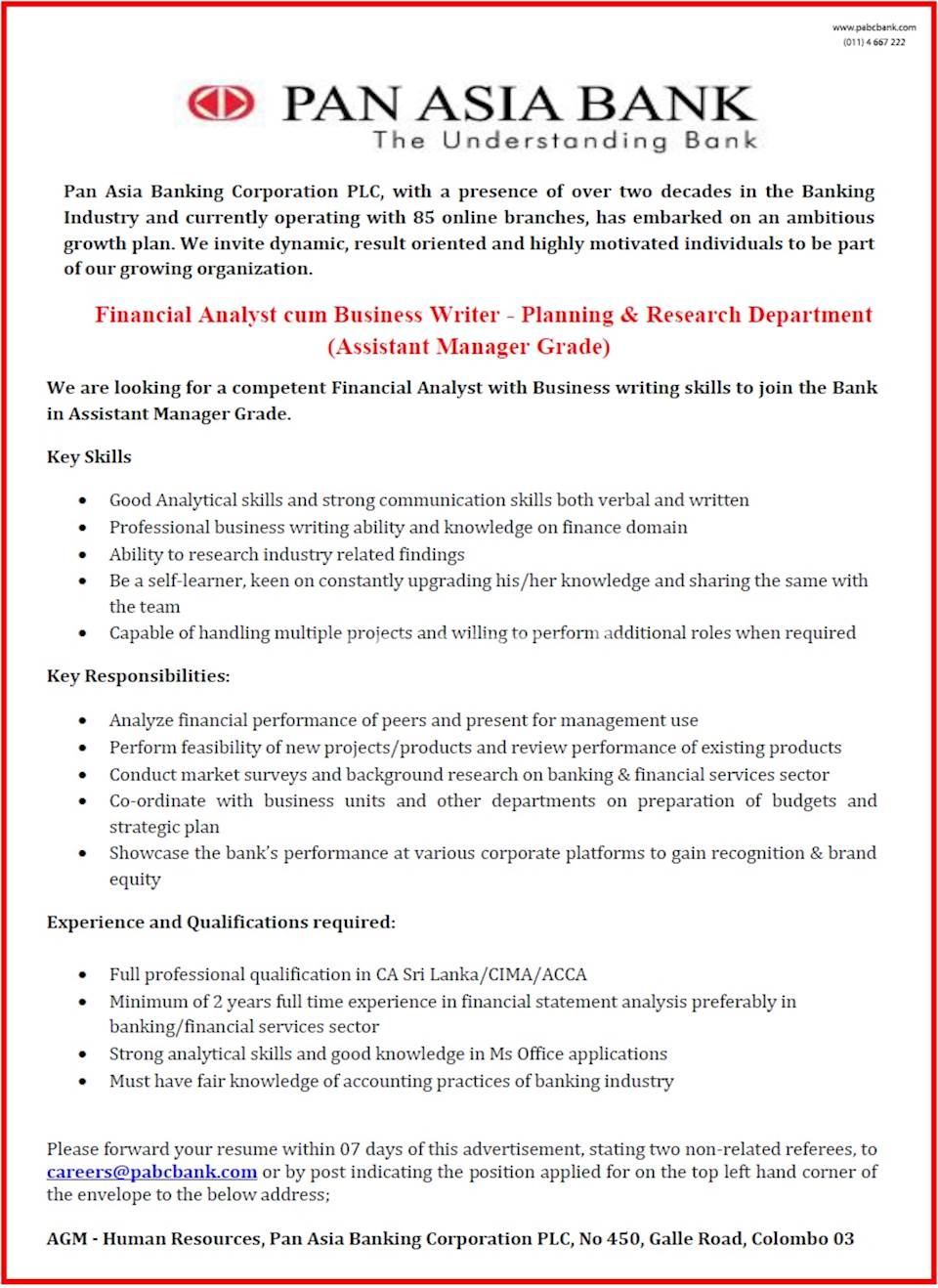

Experience required

An accountant is a professional that prepares and executes financial calculations for businesses. This typically involves creating and maintaining sales and balance sheets, as well as administering payroll. You may also manage budgets and maintain inventory. A few accountants can manage tax returns or forecast income.

An accountant's salary can vary depending on where they live, their education level, and the amount of experience they have. A master's degree in accounting, for example, can boost an applicant's salary. CPA certification can also result in a raise. Additional professional certifications may also increase an accountant's income.

Compensation

New York is the right place for you if you're looking to work in the financial and banking industry. Multinational corporations need accountants who are skilled and knowledgeable about IFRS standards. If you are a forensic accounting specialist, you will be highly in demand. This means that you will be paid more than the national average as an accountant.

Accounting salaries are dependent on experience and location. Obtaining a master's degree in accounting can help you stand out in the job market. You can increase your salary further by obtaining certifications such as the CPA (certified public accountant), or the CIA (certified intern auditor). Other factors that affect compensation levels include your level of negotiating skills, the industry in which you work, and the size of your employer.

FAQ

What's the purpose of accounting?

Accounting provides a view of financial performance by measuring and recording transactions, analyzing them, and reporting on them. Accounting allows organizations make informed decisions about how much money to invest, how likely they are to earn from their operations, and whether or not they need to raise additional capital.

Accountants record transactions in order to provide information about financial activities.

The company can then plan its future business strategy, and budget using the data it collects.

It is vital that the data are reliable and accurate.

What is bookkeeping?

Bookkeeping is the act of keeping track of financial transactions, whether they are for individuals or businesses. This includes all income and expenses related to business.

Bookkeepers track all financial information such as receipts, invoices, bills, payments, deposits, interest earned on investments, etc. They also prepare tax returns and other reports.

What's the difference between accounting & bookkeeping?

Accounting is the study of financial transactions. Bookkeeping is the recording of those transactions.

They are both related, but different activities.

Accounting deals primarily using numbers, while bookskeeping deals primarily dealing with people.

Bookkeepers record financial information for purposes of reporting on the financial condition of an organization.

They adjust entries in accounts receivable and accounts payable to make sure that the books balance.

Accountants review financial statements to determine compliance with generally accepted Accounting Principles (GAAP).

If not, they may recommend changes to GAAP.

Bookkeepers keep records of financial transactions so that the data can be analyzed by accountants.

Statistics

- In fact, a TD Bank survey polled over 500 U.S. small business owners discovered that bookkeeping is their most hated, with the next most hated task falling a whopping 24% behind. (kpmgspark.com)

- a little over 40% of accountants have earned a bachelor's degree. (yourfreecareertest.com)

- According to the BLS, accounting and auditing professionals reported a 2020 median annual salary of $73,560, which is nearly double that of the national average earnings for all workers.1 (rasmussen.edu)

- The U.S. Bureau of Labor Statistics (BLS) projects an additional 96,000 positions for accountants and auditors between 2020 and 2030, representing job growth of 7%. (onlinemasters.ohio.edu)

- BooksTime makes sure your numbers are 100% accurate (bookstime.com)

External Links

How To

Accounting for Small Business

Accounting for small businesses is one of the most important tasks in managing any business. This includes tracking income and expenses, preparing financial statements, and paying taxes. Quickbooks Online is one of the software programs that can be used. You have many options when it comes to accounting for small businesses. You must choose the right method for you, based on your requirements. Below are the top choices.

-

Use the paper accounting method. You might prefer to use paper accounting, which can be very simple. This method is very simple. You simply need to record transactions every day. A QuickBooks Online accounting program is a good option if your records need to be complete and accurate.

-

Online accounting is a great option. Online accounting makes it easy to access your accounts anywhere, anytime. Wave Systems, Freshbooks, Xero and Freshbooks are some of the most popular options. These software allows you to manage your finances and generate reports. They have many great features and are very easy to use. So if you want to save time and money when it comes to accounting, you should definitely try out these programs.

-

Use cloud accounting. Another option you have is cloud accounting. It allows you secure storage of your data on a remote server. Cloud accounting offers many benefits over traditional accounting systems. Cloud accounting doesn't require expensive hardware and software. You have better security since all your information can be accessed remotely. Third, it saves you from worrying about backing up your data. It makes it easy to share files with others.

-

Use bookkeeping software. Bookkeeping software works in the same way as cloud accounting. However, you will need to buy a computer to install the software. After you install the software, you'll be able connect to the internet and access your accounts whenever you wish. You will also be able view your balance sheets and accounts directly from your computer.

-

Use spreadsheets. Spreadsheets can be used to manually enter financial transactions. For example, you can create a spreadsheet where you can enter your sales figures per day. A spreadsheet has the advantage of being able to modify them whenever you wish without needing a complete update.

-

Use a cash book. A cashbook allows you to record every transaction. There are many sizes and shapes of cashbooks, depending on the space available. You have the option of using a different notebook for each month, or a single notebook that covers several months.

-

Use a check register. A check register is a tool that helps you organize receipts and payments. To transfer items to your check list, all you have to do is scan them in your scanner. Once there, you can add notes to help you remember what was purchased later.

-

Use a journal. A journal is a logbook which keeps track of your expenses. This is especially useful if you have frequent recurring expenses such rent, utilities, and insurance.

-

Use a diary. You can simply use a diary to keep track of your life. It can be used to track your spending habits and plan your finances.